The exit of President Bashir Assad from Syria has resulted in a bloodless revolution so far. However, could the uprising have an impact on oil markets?

![]()

The exit of President Bashir Assad from Syria has resulted in a bloodless revolution so far. However, could the uprising have an impact on oil markets?

![]()

US core inflation (year-on-year) remains stuck at 3.3% for the fourth consecutive month, a level that just won’t seem to budge. The US Federal Reserve will look at the data reports for positives and see that shelter (rent) and services inflation both rose at their slowest pace in almost three and a half years. Despite the increase in headline inflation, markets are almost certain we will see a 25bps (0.25%) rate cut next week from the US Fed but are forecasting fewer cuts in the new year as Trump takes power.

Elon Musk, the richest man in the world, has become the first person in history to have a net worth of $400bn. Tesla shares have been on a tear since election day and closed at a record high of $424.77 on Wednesday. The upcoming appointment of Mr Musk to government has been quite powerful as investors believe his mission to cut down on regulatory practices ultimately benefits his businesses in the electronic vehicle (EV) sector (Tesla) and artificial intelligence (AI) sector through his companies SpaceX and Neuralink.

The Swiss National Bank responded to the country’s weak inflation data report and the backward step in economic growth with a surprise 50bps (0.5%) interest rate cut. This takes the base rate to 0.5%, the lowest level since November 2022 and surprised markets as they anticipated a 25bps cut. The Swiss Franc weakened against the Euro after the new Chairman, Mr Schlegel, left the door open for further cuts but ruled out the likelihood of negative rates in the future. The Bank of Canada also cut interest rates by 50bps on Wednesday.

Staying on the topic of central banks, the European Central Bank (ECB) cut rates on Thursday afternoon for the fourth time this year. Interest rates are now down from the 16-year- high of 4.5% in April to 3.15%. Commentary from central banks is highly analysed by markets for insights on the future rate path, and the removal of key reference “keeping rates sufficiently restrictive” seemingly indicates an appetite for further cuts in future meetings. This cut was expected, with recent services PMI data dropping below 50 and continued weakness in economic growth.

The UK market has seemingly stalled since the Labour government took power and there was another blow to the London Stock Exchange (LSE) as equipment rental company, Ashtead, announced plans to shift their primary listing to New York. Ashtead, founded in 1984, has been listed on the LSE for the last 38 years but declared the main reason for the move was due to the US being a more natural home for the company, given that 98% of its profits are derived from the US. Shareholders are set to be consulted, and the final decision will be put to a vote, but the intent certainly highlights concerns over how attractive the UK is to investors.

UK GDP figures for October have been released this Friday morning and for the second straight month GDP shrank by -0.1%. The weak economic growth potentially stems from uncertainty over the Labour government’s Autumn budget, as the services sector flatlined and the manufacturing sector continued to decline. Chancellor Rachel Reeves admitted the GDP figures were “disappointing” but maintained the view that Labour has put policies in place “to deliver long term economic growth”.

Markets will certainly not take their Christmas break early as both the US Fed and Bank of England meet next week. We continue to emphasise the importance of diversification within portfolios, as this allows us to avoid being caught out by short term volatility and benefit from long term opportunities.

Nathan Amaning, Investment Analyst

Risk warning: With investing, your capital is at risk. The value of investments and the income from them can go down as well as up and you may not recover the amount of your initial investment. Certain investments carry a higher degree of risk than others and are, therefore, unsuitable for some investors.

Term two of Trump’s presidency could be unpredictable, as he declared he pulled off “the greatest political movement of all time”. The presidential inauguration will be held on 20th January 2025. However, Trump got straight to work nominating cabinet picks for the Senate and appointing White House advisors. A high-profile selection is hedge fund manager Scott Bessent, who will serve as Treasury Secretary and execute his 3-3-3 plan: cutting the budget deficit to 3% of GDP, boosting GDP growth to 3% through deregulation, and increasing US energy production by 3 million barrels of oil a day. Later in the month, Trump set markets on alert as he stated his intention to impose 25% tariffs on Mexico and Canada as well as additional tariffs on China. Markets believe this strong stance is a ploy to prioritise America in trade talks but if imposed the tariffs will likely have inflationary impacts.

While the US election took centre stage, there was a raft of economic and corporate data during November. The US Federal Reserve’s preferred measure of inflation, personal consumption expenditure (PCE) increased 0.2% (month-on-month) and rose to 2.3% (year-on-year). Core PCE (excludes food and energy costs) showed an even stronger reading at 2.8% (year-on-year). Inflation is still within reach of the 2% target and as such, bets are still on that the US Fed will continue its rate-cutting path when they meet for the final time this year in December.

It was corporate earnings season as Nvidia, the world’s largest company, showcased impressive growth. They announced record revenues of $35bn and net profit margins of 55%, up 7.9% from the previous year. The continued strong performance highlights Nvidia’s dominance in artificial intelligence (AI). However, markets were slightly concerned with the delayed timing and performance of their new Blackwell GPU chips, which were rumoured to be overheating. The company quickly addressed these worries, stating all design issues had been resolved and that demand for the chips has exceeded their expectations.

In the UK, the Bank of England (BoE) cut interest rates by 25bps (0.25%) to 4.75%, marking its second cut of the year. The decision was almost unanimous among policymakers with an 8-1 vote in favour of the cut. The decision was driven by the positive fall in inflation to 1.7% in September. Inflation figures for the previous month revealed an expected spike to 2.3% following the increase in the energy price cap by 10% to £1,717 on average. Given the recent pickup in inflation and the expected inflationary impact of the Autumn Budget, the market is not anticipating a rate cut at the next BoE meeting.

The Labour governments budget was announced on the 30th of October, but the effects were felt before and after as speculation over which taxes would be increased led to UK businesses and consumers to hold back on spending. UK businesses will bear the brunt of increased national insurance tax. Retail sales suffered in the build up to the budget as they fell to -0.7%, however we can expect to see a rebound as consumers took advantage of Black Friday shopping on the last Friday of the month.

Over the month, Japan’s economy showed signs of a modest recovery. Q3 GDP was positive at 0.2%, the second consecutive positive quarter and inflation fell to 2.3% (year-on-year). The Japanese government also announced a significant stimulus package worth $140bn which includes energy & fuel subsidies in addition to cash handouts for low-income households. Japan’s Prime Minister, Mr Shigeru Ishiba, who has only been in power since 1st October, has made a bold promise to spend 10 trillion yen through to 2030 to boost Japan’s semiconductor and artificial intelligence sectors, helping the nation regain its technology edge.

Bitcoin made the most remarkable move over the month, gaining nearly 40% and closing at highs of $99,000. The rally was kickstarted by Trump’s strong views on deregulation and also his comments on potentially creating a bitcoin reserve. A new DOGE team has been created, not the cryptocurrency but the Department of Government Efficiency, led by the richest man in the world, Elon Musk. The primary goals are to reduce wasteful government spending and eliminate unnecessary regulations.

To summarise the month of November there was a range of political and economic developments that shifted markets. US equity markets benefitted the most as Russell 2000 (US Small Cap) rose almost 11%. The US Federal Reserve and Bank of England both cut rates, but markets are split on whether both central banks (or just one) will make the final rate cut of the year in December.

Nathan Amaning

Investment Analyst, Raymond James, Barbican

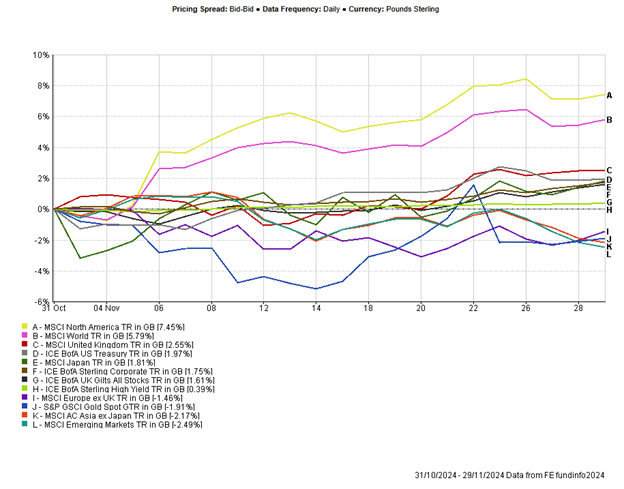

Appendix

5-year performance chart

Risk warning: With investing, your capital is at risk. Opinions constitute our judgement as of this date and are subject to change without warning. Past performance is not a reliable indicator of future results and forecasts are not a reliable indicator of future performance. This article is intended for informational purposes only and no action should be taken or refrained from being taken as a consequence without consulting a suitably qualified and regulated person.

British house prices rose by 3.7% in November (year-on-year) reflecting the largest rise in exactly two years. The Bank of England (BoE) also reported the most mortgage approvals by lenders in the last month since August 2022. The increased housing activity stems from the Labour party’s decision to end stamp-duty reliefs at the beginning of the new tax year in April 2025, bringing forward house buyers purchases and hence boosting house prices in the short term.

In just twelve days, the BoE will meet again for the final time this year to decide whether a pause is needed in their rate-cutting path. Inflation figures for November will be released the day before the meeting, and the BoE will fully consider other leading indicators. Firms are reacting to the national insurance tax rises and may raise prices instead of cutting jobs, which would be inflationary. BoE Governor Andrew Bailey remained coy on their next move stating there was still “distance to travel” to control inflation.

The European Central Bank will meet next Thursday and has already cut interest rates three times since June. Finnish policymaker Olli Rehn has spoken ahead of the meeting, explaining the increased justification he sees for cuts. He pointed out weakening economic growth around the Eurozone and rising inflation, which is still within touching distance of the 2% target.

After the debacle over the French budget last week, it was expected that Premier Michel Barnier would be forced out of parliament. On Wednesday, 331 French members of parliament voted no confidence, forcing Barnier’s resignation. His tenure, beginning only four months ago is the shortest of any premier in 66 years. President Macron must act quickly in his search for a new prime minister, one strong enough to push a new 2025 budget through a deeply divided government.

Across the Atlantic ocean, US services sector PMI’s slowed to 52.1 for November following strong results over the previous months of September and October. A figure above 50 means the sector remains in the expansionary zone, which is certainly a positive reflection on the US economy. On Wednesday the US Fed released the last beige book for the year, which provides insight into economic conditions across the twelve federal districts. The takeaway from the report is that economic growth was stable and growing across most districts; however, businesses were uneasy about the incoming tax and regulation that will be implemented in the New Year as Trump takes the hot seat.

US non-farm payrolls was released this Friday afternoon with 227,000 jobs added in November. This shows a rebound from the 36,000 jobs in the previous month which was heavily affected by the strikes and hurricane Milton that passed over Florida.

We’ve previously written about the artificial intelligence company Super Micro Computer, as they are late in filing their annual and quarterly earnings reports. Their previous auditors Ernst & Young, resigned in October following this however a special committee announced this week “no findings of fraud or misconduct”. This news led the share price rally of almost 25% over the week, however the company is not out of the woods yet. Super Micro’s new auditor, BDO has yet to certify the company’s earnings, and the company is on the timer to deliver their financial reports or face being delisted from the Nasdaq.

We expect next week to be as busy as this week, with inflation reports from the US and Germany, UK GDP and central bank decisions from the European Central Bank and Canada. A given possibility may be the continued rise of Bitcoin as it breached the $100,000 mark on Thursday, up almost 3% for the week.

Nathan Amaning, Investment Analyst

Risk warning: With investing, your capital is at risk. The value of investments and the income from them can go down as well as up and you may not recover the amount of your initial investment. Certain investments carry a higher degree of risk than others and are, therefore, unsuitable for some investors.

Our European Strategist, Jeremy Batstone-Carr considers the potentially seismic effect of the US election result on global markets, and China in particular, including some possible effects of the much-touted trade tariffs that have been promised for the coming year. And as the effects of the UK Budget become clearer, what is the potential for domestic inflation?

![]()

Starting the week in the UK, Bank of England (BoE) Deputy governor, Clare Lombardelli made her first speech since joining the committee in July. With UK inflation rising to 2.3% in October, Ms Lombardelli appeared most concerned that inflation may continue to rise above expectations due to the spike in services inflation and persistently strong wage growth. Judging by her commentary it would be hard to see her backing a further rate cut at the next policy meeting. The impact on the economy of imminent Trump tariffs is also set to be discussed during the next meeting.

There was a blow to the London stock exchange with Just Eats’ latest announcement to delist from the exchange at the end of the year and trade in Amsterdam only. They stated their reasons for delisting due to “administrative burden, complexity, and costs” but more worryingly were concerned by “low trading volumes and liquidity”. This is undoubtedly a setback in the Labour government’s attempts to repair UK’s reputation as a business hub. Recent M&A activity has seen a reduction in the number of UK listed companies and this week saw a resurgence in M&A activity. Aviva had a bid rejected for Direct line, while yet another US private equity firm bid for a UK business, offering £338m for Loungers. The bid activity was not over there, with Australia’s Macquerie bidding for UK listed waste firm Renewi. It seems foreign buyers are taking advantage of the recent weakness in sterling, which makes UK companies more attractive, coupled with already depressed valuations.

Stellantis is a global car manufacturer owning companies such as Alfa Romeo, Peugeot, Fiat and Vauxhall. Vauxhall is set for a reshuffle as they are set to close their Luton factory putting 1,100 jobs at risk. There is also set to be a consolidation at their Ellesmere site, just one hour away from the Luton site, as Stellantis are investing £50m into an electric vehicle (EV) hub. They are currently under pressure to speed up their transition to EVs as 22% of car sales must be purely electric or risk a regulatory fine.

German headline inflation has risen in November from 2% to 2.2%. Core inflation (excludes energy and food prices) also rose to 3% adding pressure to Europe’s largest economy. German Chancellor, Olaf Scholz, has officially been named as the Social Democrat’s candidate ahead of German elections next February following the collapse of the coalition with the Greens and Democrats earlier this month. He has his work cut out to bring down high energy prices and modernise Germany’s manufacturing heavy economy.

In France, the government coalition is on the brink of collapse as Prime Minister Barnier has suffered blowback from his latest budget proposal. Barnier aimed to rein in the country’s public debt deficit by €60bn through spending cuts and tax hikes but has since backtracked, removing a proposed tax increase on electricity. Marine Le Pen, leader of the far-right National Party is expected to vote for a motion of no confidence which would cause the government to collapse. French equity markets have reacted negatively to the news, down -1.5% for the week.

US PCE is a slightly different measure of inflation and is highly regarded as the US Federal Reserves preferred measure. On Wednesday US PCE (year-on-year) rose to 2.3% for October, reflecting an increase in inflation away from the 2% target. Incoming President Donald Trump spoke earlier this week and spooked markets with his strong vow to implement a 25% tariff on all Mexican and Canadian products followed by an additional tariff on Chinese products. The US Federal Reserve are still expected to deliver a further 25bps (0.25%) cut in their December meeting, but a pause may be on the cards in 2025 in order to assess Mr Trump’s policies.

Next week, we will receive US non-farm payrolls which is expected to bounce back following the surprisingly low 12,000 jobs created in October. In a controversial move, Australia have passed a bill that bans children under 16 from social media apps such as Facebook, Instagram and TikTok with concerns around mental health of young people. It will be interesting to see if any other countries follow Australia’s lead, and what, if any, impact it has on the social media companies revenues.

Nathan Amaning, Investment Analyst

Risk warning: With investing, your capital is at risk. The value of investments and the income from them can go down as well as up and you may not recover the amount of your initial investment. Certain investments carry a higher degree of risk than others and are, therefore, unsuitable for some investors.

With UK headline inflation at 2.3% (year-on-year) for October and core inflation (excludes food and energy prices) rising to 3.3%, inflation rose back to a six-month high and puts the Bank of England (BoE) on alert. The rise from energy prices had been expected with the quarterly energy price cap rising 10% to £1,717 on average and to add to the “triple dose of bad news”, services inflation rose to 5%. Since Labour’s budget the market has become more concerned about inflation, estimating that it will drift higher to end the year. It’s been 15 days since the BoE cut interest rates to 4.75% and the probability of a further cut in the month of December has fallen to 16%.

UK retail sales for October have been released early this Friday morning and again disappointed beyond market expectations. Month-on-month sales were predicted to fall 0.3% but came in at -0.7% and the year-on-year figure falling to 2.4% from the previous 3.2%. In the build-up to last month’s budget and speculation over which taxes may be increased, consumer confidence was certainly affected, and shoppers were more reluctant to spend. Weather conditions have taken a turn this week with extreme colds and snow in parts of the country however we can expect a rebound in retail sales to end the year with Black Friday approaching next week and Christmas spending to begin in December.

Similar to the UK, Eurozone inflation has been on the rise in the last month. Headline inflation rose to 2%, which is in line with the European Central Bank’s (ECB) target. When the ECB met in October, they maintained the belief of a short-term inflationary uptick before a gradual decline in 2025, so we may see a pause in their current interest rate cutting cycle at their next meeting. ECB Vice President, Luis de Guindos is awaiting to hear if incoming US President Trump will impose any tariffs on Europe but has said he expects tariffs to hurt economic growth within Europe rather than be inflationary.

Rising geopolitical activity between Russia and Ukraine has led Gold to have its best weekly gain in over a year. Oil is also back up to $70 a barrel rising 5% for the week as the Euro vs Dollar fell to $1.04, its lowest level since December 2022.

Over in the US, it was expected that 220,000 people would file for unemployment benefits last week however that figure came in at 213,000, a seven-month low. The impact of Hurricane Milton in Florida and strikes certainly distorted job growth figures in October so we are seeing that rebound in hiring activity.

It was Nvidia’s earnings report day on Wednesday as the world’s largest company reported revenue of $35.08bn for Q3, beating expectations of $33.15bn. The company also projected that revenue was set to increase by 70% in the next quarter. The bar has been set extremely high for Nvidia to consistently beat expectations and Nvidia’s outlook on AI chip supply timing and capacity initially disappointed investors. There has since been a mini recovery, and the share price is up 1.2% for the week.

It has been a positive week in markets with equities having a strong end to the week, most notably US small cap. European markets were impacted by political instability in Germany in addition to slower recovery projections for the manufacturing sector. The importance of diversification across regions, asset classes and sectors cannot be overstated as we aim to enhance the resilience of portfolios whilst capturing long term opportunities.

Nathan Amaning, Investment Analyst

Risk warning: With investing, your capital is at risk. The value of investments and the income from them can go down as well as up and you may not recover the amount of your initial investment. Certain investments carry a higher degree of risk than others and are, therefore, unsuitable for some investors.

Following on from the US Federal Reserve cutting interest rates last week, a range of US inflation data was released this week. Headline inflation picked up from 2.4% to 2.6%, which was in line with expectations. Housing costs (rent), air fares and used cars all contributed to inflation, while gasoline prices dropped. Core inflation (excludes food and energy prices) remained steady at 3.3% and will no doubt cause concern for the US Fed, given its elevated level. The combination of inflation data, coupled with words from Fed Chair Jerome Powell led to markets lowering the probability of an interest rate cut in December from 80% to 60%. US government bonds have been weak over the last six weeks and the inflation data did little to reverse this trend. The yield on the 10-year US treasury bond is now approaching 4.5%, as investors grow concerned around the inflation outlook for the US, coupled with significant fiscal spending. The trend has not been unique to the US, with UK government bonds also having a soft patch in recent weeks. Government bonds have continued to exhibit high levels of volatility since 2022, yet at current yield levels, offer the prospect of inflation beating returns.

The UK was in the spotlight this week with Chancellor Rachel Reeves speaking in her Mansion House address, her first speech to prominent business leaders and financiers. It is clear that Reeves is keen on removing some of the regulation and red tape that has potentially held back investment and growth. She stated, “The UK has been regulating for risk, but not regulating for growth”. She also announced considerable pension reform, aiming to create less, but much larger pools of pension capital which can be deployed into infrastructure and private markets. While there was limited mention about public market reform, this could be announced in 2025, with the aim of stemming outflows from UK equities.

There was disappointing news for the Chancellor to wake up to on Friday morning with UK GDP data underwhelming. For the third quarter of 2024 the UK economy only grew by 0.1%, with GDP falling by -0.1% for the month of September. The data was below expectations, with the uncertainty created by the autumn budget deemed as a significant reason for the lacklustre growth. Despite the data, the market is still viewing an interest rate cut in December as unlikely, with the likelihood of the next cut being delivered in February 2025.

Staying with the UK, employment and wage data was also released this week. Average earnings index, which tracks the change in prices businesses and governments pay for labour, including bonuses, rose more than expected to 4.3%. This level of wage growth is above current inflation levels and should help support consumption in the economy. Despite wages rising faster than expected, the unemployment rate surprisingly jumped to 4.3%, from 4.1%.

After a strong run, gold has stumbled this week, falling below $2,600 an ounce, a likely unwind of pre-election hedges. It’s not the only weak commodity, with brent crude oil slipping to $72 a barrel this week.

At a currency level the recent trend of US dollar strength prevailed throughout the week. The USD:Yen rate is back above 155, while sterling dipped below 1.27 against the greenback on Friday, its lowest level in over three months.

The “Trump Trade” has gotten into its swing as Bitcoin has hit a historic high of $88,000, rallying almost 30% since election day. This has been fuelled by investors anticipating a more favourable regulatory environment for cryptocurrencies. Tesla shares have risen almost 25% in the same period as CEO, Elon Musk, was announced head of a new department, Department of Government Efficiency. The acronym “DOGE” is already raising eyebrows but his role entails slashing excess regulations, cutting wasteful government expenditure and restricting federal agencies.

Looking ahead to next week, UK inflation data will be one to watch. Headline inflation is expected to rise to 2.2%, from the current level of 1.7%, in part due to the increase in the energy price cap at the start of October.

Andy Triggs, Head of Investments

Risk warning: With investing, your capital is at risk. The value of investments and the income from them can go down as well as up and you may not recover the amount of your initial investment. Certain investments carry a higher degree of risk than others and are, therefore, unsuitable for some investors.

There have already been many column inches dedicated to covering the budget. As such, I will just touch on the market impact. In terms of government bonds, after an initial rally, UK government bonds sold off following the budget and continued to sell-off on the final day of October. This means UK borrowing costs are going up, not ideal given Labour’s need to increase borrowing to fund their spending plans. With the Office for Budget Responsibility (OBR) stating they expect inflation in the UK to be higher post-budget, the market has priced out some of the expected interest rate cuts. There has been a trend of developed market government bonds selling off in October, so the movement may not be fully attributable to the budget. Equity markets had a mixed response to the budget. The winner on the day was the UK AIM market, which rallied over 4%. This part of the market had sold off into the budget, with concerns around the removal of certain inheritance tax benefits. However, the changes announced were less punitive than expected, leading to an immediate relief rally. The mid-cap focused UK index marginally advanced on the budget day, while the large-cap index closed lower.

Staying with the UK, earlier in the month there was positive inflation data. Headline inflation dropped to 1.7%, lower than expected, while services inflation fell from an annual rate of 5.6% to 4.9%. The positive shift in both headline and services inflation has opened the door to UK interest rate cuts in both the November and December Bank of England (BoE) meetings. The fly in the ointment now is whether the inflationary budget will cause the BoE to pause its rate-cutting journey.

Over in the US, the presidential election (5th November) dominated headlines. Despite the uncertainty surrounding the election outcome, US equities powered on, reaching a 47th all-time high during October. After a summer lull, the mega cap technology and artificial intelligence focused companies regained their poise to post a strong month. The star performer from the so called “Magnificent Seven” stocks was Tesla, which rallied over 20%, after a strong earnings report. Founder and largest individual shareholder, Elon Musk, saw his net wealth rise by over $30bn in two days because of the rally, taking his overall wealth to $277bn, cementing his place as the world’s richest person.

There was positive inflation data in the US, with headline inflation coming in at 2.4%, the lowest reading since February 2021. The continued decline in inflation helps make the case for further interest rate cuts from the US Federal Reserve. Two central banks that are further on in their rate cutting journey are the Bank of Canada (BoC) and European Central Bank (ECB). The BoC delivered a 0.5% cut in October, meaning they have already reduced interest rates by 1.25% over a matter of months. The ECB delivered their third cut of 2024, lowering rates by 0.25% for the second meeting in a row. The market is currently pricing in cuts from both the US Federal Reserve and the Bank of England in November.

After the excitement of September, emerging market and Asian equities were much more subdued. There have been concerns about the Chinese authorities’ abilities to deliver on their planned stimulus measures and even if they do, the market is unsure whether it is enough to turn round a flagging property market and struggling economy, hamstrung by poor demographics. As a result, Chinese equities fell during the second half of the month as investors pared back their bets on the world’s second-largest economy. We have seen companies that rely on China as an end market struggle of late. Within the luxury goods sector, companies such as Burberry have blamed Chinese weakness for poor results. UK-listed medical technology company Smith & Nephew also pointed to China as a reason for disappointing Q3 results.

Gold had another impressive month, making new all-time highs during October, with the price approaching $2,800 an ounce. The price of the precious metal has outperformed most equity and bond markets, rallying approximately 30% in 2024. Although not covered in the chart, silver has outperformed gold this year, and while the gold price is at all time-highs, silver is still close to 50% off its all-time high. Silver is often seen as more cyclical than gold, due to its more commercial use, and doesn’t offer the same diversification properties within a typical multi-asset portfolio.

At a currency level, we saw a resurgent US dollar after a few months of weakness against a basket of currencies. Against sterling, this meant it moved from around 1.34 to 1.30. Given the large fiscal deficit currently being run by the US, one could argue that the US dollar might weaken going forward. However, as the world’s reserve currency, and with no viable alternative, there is always likely to be demand for the greenback currency.

The end of October 2023 kickstarted a strong rally into the end of the year, with nearly all gains made during the year, occurring in the final two months. It was a reminder that patience is needed when investing, and that returns can be lumpy, but substantial at times. With events like the budget now over, and the US election soon to pass, some of the uncertainty looking over markets will be fully removed, which could support risk-taking once more.

Andy Triggs

Head of Investments, Raymond James, Barbican

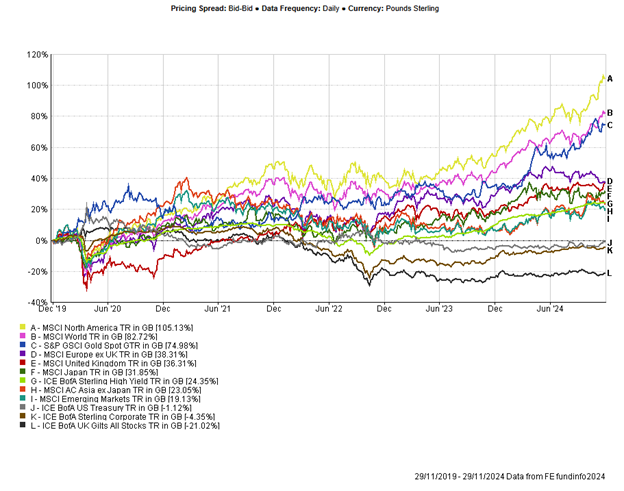

Appendix

5-year performance chart

Risk warning: With investing, your capital is at risk. Opinions constitute our judgement as of this date and are subject to change without warning. Past performance is not a reliable indicator of future results and forecasts are not a reliable indicator of future performance. This article is intended for informational purposes only and no action should be taken or refrained from being taken as a consequence without consulting a suitably qualified and regulated person.

The main event this week was the US election. In what was expected to be a very closely run election, Republican Donald Trump won the presidential election, including the popular vote, securing nearly five million more votes than Kamala Harris. The Republicans also secured a majority in the senate. It’s still not finalised who will control the House of Representatives, although there is the chance for the Republicans to secure a clean sweep. There were big moves in markets, particularly the US on Wednesday as the results poured in. The biggest winner was the US equity market, with small cap equities performing particularly well, rising over 5% on the day. While equities rallied, US government bonds sold off aggressively. This was likely driven by the view that some of Trump’s policies, such as tariffs, could be inflationary, which would potentially delay interest rate cuts. The US dollar advanced against most major currencies, strengthening by around 1.5% against sterling. Commodities were under pressure, potentially due to concerns about China on the back of Trump tariffs. Equity returns outside of the US were muted on Wednesday. After an initial surge in early trading, European and UK markets gave up most of their returns in the afternoon session.

Yesterday the Bank of England (BoE) met for the first time since Labour’s first budget. As expected, the BoE carried on their interest rate cutting journey, reducing rates by 0.25% to 4.75%. Eight of the nine voting members supported the cut. The accompanying statement by the BoE pointed towards a “gradual approach” to reducing interest rates going forward.

By Thursday evening the US Fed had joined the BoE in reducing rates by 0.25%, following on from their bumper 0.5% cut in September. Governor Powell’s follow up comments to the cut appeared very hawkish, and it’s clear the US Fed will be data dependant and currently don’t see the need for deep cuts going forward. The interest rate cuts will favour some small businesses who typically have floating rate debt and therefore immediately feel the benefit of lower interest rates.

There were unscheduled political events in Germany this week. Chancellor Scholz fired the finance minister, after which two colleagues resigned, leading to the effective breakdown of the German coalition government. There is likely to be snap elections in the New Year in Germany now, which adds a level of uncertainty to Europe’s largest economy. The country is far from firing on all cylinders, with the economy predicted to have zero growth in 2024, while the IMF expects Germany to grow by only 0.8% in 2025. Increased energy costs since Russia’s invasion of Ukraine, coupled with China weakness has hit the manufacturing hub in Germany very hard.

After a strong week, Nvidia once again became the world’s largest company, with its market capitalisation rising above $3.4 trillion. Big technology companies in general saw strong share price movements in the wake of the election. However, given Trump’s previous comments around increased regulation in the technology sector and the sector’s bias against conservatives there is certainly a risk to this sector under a Trump regime.

The passing of the UK Budget and US Election means we are now through two events that created a great deal of uncertainty. Regardless of the results and outcomes, markets can now begin to price the risks and hopefully move forward. At a portfolio level we work hard on trying to spread risk, and typically try to avoid binary events having big impacts on portfolios.

Andy Triggs, Head of Investments

Risk warning: With investing, your capital is at risk. The value of investments and the income from them can go down as well as up and you may not recover the amount of your initial investment. Certain investments carry a higher degree of risk than others and are, therefore, unsuitable for some investors.

The value of investments, and the income derived from them, can fall as well as rise. You may get back less than invested. Past performance is not a reliable guide to future returns.