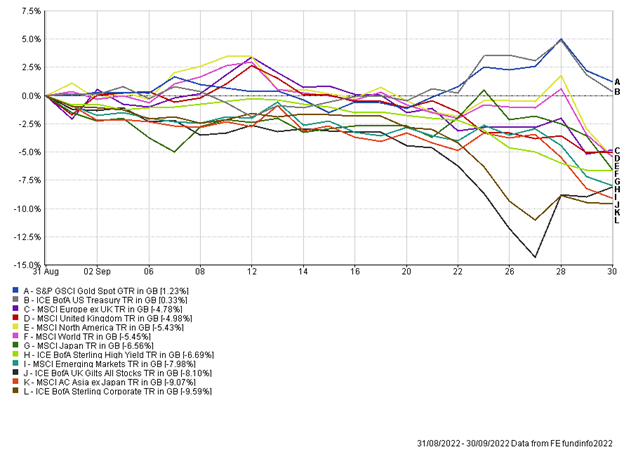

It has been somewhat of a rollercoaster ride in markets this week with numerous economic data releases from the UK and US, Chinese whispers around UK parliament on the future of the mini budget and historic equity intra-day reversals.

The UK has certainly been the topic of conversation for all the wrong reasons over the period since Liz Truss became Prime Minister in early September. However, there was some good news in the form of jobs data on Tuesday with the unemployment rate falling to 3.5%, beating forecasts. This was the lowest unemployment rate since February 1974, however, there has been a sharp rise in the number of “economically inactive” workers – not employed or looking for work.

We saw the results of UK GDP on Wednesday; GDP month-on-month came in at -0.3% whilst year-on-year came in below expectations at 2% (forecast 2.4%). Growth within the UK’s economy is set to continue to slow as surging inflation continues to hit households, and the Bank Of England (BoE) looks set to continue to raise interest rates sharply in response. The BoE also spoke earlier this week, being very clear that the gilt-buying programme was set to stop this Friday. This sent the pound plunging to $1.10 and gave liability driven investment managers three days to shore up enough cash reserves for pension fund clients to meet margin calls.

There has since been a rally in UK markets as rumours began to spread of Chancellor Kwasi Kwarteng and Prime Minister Liz Truss considering a total U-turn of the tax cuts within the mini budget. The pound traded above $1.13 against USD on Friday’s opening. Last week they reversed their intended plan of cutting the tax rate of 45% to 40% and it’s been reported that a reversal of more of the mini budget will calm market turbulence. Mr Kwarteng has cut short his visit to the US which could confirm the rumours, it’s worth keeping an eye out on this!

US September inflation numbers were announced yesterday. Inflation YoY came in slightly ahead of expectations at 8.2% versus 8.1%. Core inflation, which excludes food and energy prices came in at 6.6% versus 6.5%. Initially markets fell on the data, but we saw a dramatic recovery into closing. The S&P 500 closed in excess of 2% up, having been down over 2% at the start of the day. This is only the fifth time in history such an event has happened. US government bond yields rose on the inflation news, with markets believing the US Fed will continue to raise rates in an effort to bring down persistently high inflation. The headline yield on the 10-yr US Treasury bond breached 4% – the highest yield since 2009. While it currently feels like one way traffic in bond markets, the yields now available for investors are looking very attractive.

Switching focus to Europe, France has been at a standstill with a week-long strike. French unions walked away from wage talks with oil major Total, dashing hopes for an end to the standoff that has disrupted everyday life in France with petrol stations running dry. Unions have set a bar chasing a 10% wage rise, citing inflation and windfall profits made by the company from the energy crisis. The French Government has since stepped in urging Total to hike salaries accordingly.

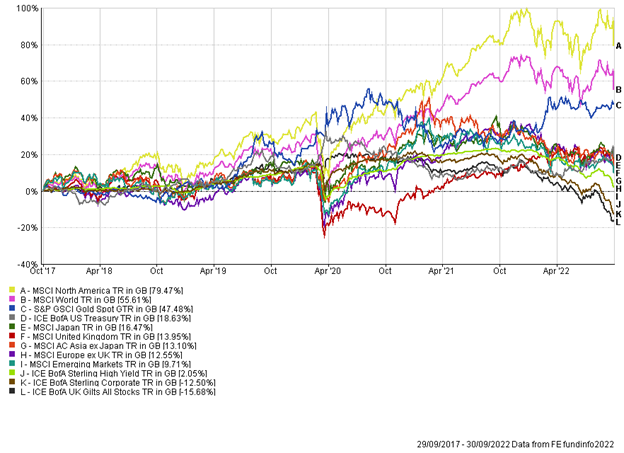

This paragraph echoes messages from previous weekly roundups, with a reminder that we continue to focus on being long-term investors and aiming to seek balance and diversification within portfolios. As we have seen this week, anything can happen in markets in a matter of hours or days. However, we expect fundamentals to be the main driver of markets in the long run and by focusing on this we can take advantage of short-term moments.

At the time of writing, it’s just been announced that Prime Minister Liz Truss will be holding a press conference this afternoon, however Chancellor Kwasi Kwarteng will not be present.

Nathan Amaning, Investment Analyst

Risk warning: With investing, your capital is at risk. The value of investments and the income from them can go down as well as up and you may not recover the amount of your initial investment. Certain investments carry a higher degree of risk than others and are, therefore, unsuitable for some investors.