Our Spring Budget Newsletter breaks down the Chancellor’s recent announcement, outlining what it means for you and helping you to plan for the new tax year – which is almost upon us.

![]()

Our Spring Budget Newsletter breaks down the Chancellor’s recent announcement, outlining what it means for you and helping you to plan for the new tax year – which is almost upon us.

![]()

There were other major announcements, such as National insurance (NI) being cut by an additional 2%, the earnings threshold for child benefit increased to £60,000, the windfall tax on oil and gas companies extended to 2029 and the higher rate of capital gains tax on residential property reduced from 28% to 24%. Overall, there were no major surprises in the Budget, and markets seemed fairly pleased with the outcome, with both UK equities and UK government bonds rallying on Wednesday.

This week we saw our latest example of mergers and acquisitions (M&A) in the UK as Nationwide agreed to purchase Virgin Money in a £2.9 billion deal. Just last month Barclays bank purchased the banking operations of supermarket Tesco for £600m. Many banks currently trade on low valuations, despite increasing profits recently and having strong balance sheets, as such the trend for M&A could continue going forward. The same is true for the whole UK market, where there has been a recent pick up in M&A activity, largely driven by foreign buyers picking off cheap UK assets. While this provides a short-term boost for investors, over the long-term it could damage the UK market as companies are picked off.

The European Central Bank (ECB) met for their second meeting of the year on Thursday and as expected they held the base rate firm at 4.5%. Investor expectations for the first-rate cut has now been pushed back to June as ECB President, Christine Lagarde, mentioned cuts were not discussed this meeting but the “dialling back of our restrictive stance” will begin in following meetings. Incoming data releases will be pivotal towards the rate decision as inflation falls towards the 2% target, while the ECB will also evaluate Q1 wage data before making their move. We have previously written that it is likely the ECB will not cut before the US Fed make their first move, for fear of devaluing their currency, however, the data may force the ECB’s hand to act sooner rather than later.

US Non-farm payroll data was announced this afternoon with 275,000 jobs being added to the economy in February despite the market expectation of 200,000 jobs. This shows the continued resilience in the labour market, highlighting the strength of the US economy. The US Fed will consider all data points before deciding to cut interest rates later this year.

Apple have had a tough start to the year. They have just been hit with a €1.8bn EU antitrust fine and now they face another dilemma as iPhone sales in China have fallen 24% (year-on-year) over the first six weeks of 2024. China contributes just under a fifth of total sales for Apple. Huawei are China’s leading tech giants in smartphones, and they have seen sales rise by 64% over the same period. Apple are one of the “Magnificent Seven” stocks that contributed to the extraordinary US market performance in 2023, however it appears that their bubble may have burst.

Super Tuesday is a term commonly known in the US as the beginning of the race for the White House during an election year. Voters in 15 states chose their candidate to run for Presidency and the expected winners were no surprise as Joe Biden and Donald Trump emerged as front runners. Republican Nikki Haley did her best but came short in convincing the party that it was time to dump Trump.

It was a largely positive week for equity and bond markets. After a stellar end to 2023, UK assets had started the year on the back foot but have begun to erase earlier falls. One asset class that has regained its shine has been gold, which is approaching all-time highs once again.

Nathan Amaning, Investment Analyst

Risk warning: With investing, your capital is at risk. The value of investments and the income from them can go down as well as up and you may not recover the amount of your initial investment. Certain investments carry a higher degree of risk than others and are, therefore, unsuitable for some investors.

In this month’s Market Commentary, Raymond James European Strategist, Jeremy Batstone-Carr, looks back on the strong performance of many of the world’s leading markets, the ongoing popularity of investment in artificial intelligence, and whether this current stock market strength can last.

![]()

In the UK, house mortgage approvals have risen in January to 55,227. This was a surprise as it beat market expectation of 52,000 and signals the largest rise in approvals since October 2022. Recovery of the UK housing market is underway following the squeeze of higher restrictive policy environment over the past 2 years. The Bank of England (BoE) are expected to cut interest rates heading into Q2 2024, and mortgage rates will follow the trend. Rates on the two-year and five-year for mortgages have also continued to fall from their peak last July. The government’s latest proposal of a 99% mortgage scheme in an attempt to encourage first time buyers has also received mixed reviews.

Shein is a Chinese clothes retailor that has in recent years gained huge popularity through apps such as YouTube and TikTok. It was downloaded twice as many times as Amazon’s app over 2023 making it the world’s most popular shopping app. The reason we bring it up is because this week, UK Chancellor Hunt held talks with Shein in a push for the company to list on the London Stock Exchange. A listing the size of Shein’s would be a huge accomplishment for the UK, who have struggled to attract IPOs and retain promising companies who have listed in the US. Bloomberg have estimated the float could total up to $90billion!

US inflation figures were out on Thursday as the US Fed’s preferred measure of inflation, PCE, was announced. Headline PCE in January (year-on-year) fell to 2.4% from the previous 2.6% in December as Core PCE also fell to 2.8%, 10bps lower than December. The timing of the first interest rate cut by the US Fed remains uncertain and recent policymaker commentary have indicated they are in no rush to make that first cut.

Japan inflation figures were also released this week as headline inflation (year-on-year) was 2.2% in January, falling from 2.6% the previous month. This is the third consecutive month inflation has fallen and as core inflation hit the central banks target of 2%, the end of negative interest rates is a possibility in the following month of April. Energy costs falling has been a significant contributor to the slowdown as government subsidies assisted in curbing oil and gas bills. The challenge for the Bank of Japan (BoJ) will be to balance falling inflation but also tackle the two consecutive quarters of falling GDP alongside the weak Yen. Off the back of positive inflation figures, Japan’s Nikkei approaches the 40,000 level.

Next week is the March Budget as we eagerly await to see what measures will be announced. This event is largely regarded as Rishi Sunak and Chancellor Hunt’s last opportunity to sway the imminent election back towards the Conservatives.

Nathan Amaning, Investment Analyst

Risk warning: With investing, your capital is at risk. The value of investments and the income from them can go down as well as up and you may not recover the amount of your initial investment. Certain investments carry a higher degree of risk than others and are, therefore, unsuitable for some investors.

The Japanese equity peak that was attained in 1989 was often referred to as the “iron coffin lid” as it became the symbol of Japan’s many years of economic stagflation. However, 34 years later that lid has been lifted, helped by a falling Yen which has boosted the exporters, while foreign investors have fled Chinese equities and found solace in Japan. Japan’s government will also have seen the benefits of their subsidised scheme, “savings to investments”, which allowed domestic households to invest into a Japanese NISA (Nippon Individual Savings Account). A scheme like this would certainly benefit the UK market and something that the Chancellor seems to be exploring ahead of the March Budget.

While the word “recession” can sound scary, we must remember that equity markets are forward-looking mechanisms, discounting the future as opposed to present and it is why equity markets often bottom and recover well before the economic low. Indeed, in the UK, the mid-cap index has historically delivered returns of around 20% in the following 12 months once a technical recession has started.

China appears to be making attempts to revive their property market and broader market as on Tuesday they announced a reduction in their benchmark mortgage rate. A 25-bps cut to their five-year loan prime rate is the largest cut since the rate was introduced in 2019 and now stands at 3.95%. Investors still however seem to be waiting for further support measures as although the rate cut was immediate, existing mortgage holders will not benefit from a loan repayment reduction until next year. A follow-up of cash injections into lenders, housing projects and developers is widely expected.

A lot of discussion around US markets over the past few months has been around the “Magnificent Seven” but we are certainly seeing Nvidia’s sway over the market growing at an absurd rate. Nvidia embodies the artificial intelligence movement as the semiconductor company’s chips are considered market leading. On Wednesday, Nvidia reported record revenues of $22bn for Q4 and full year revenue for 2023 of $60bn, leading to a market rally as the S&P 500 rose 2% and tech-heavy Nasdaq rose 3%. Nvidia added $250bn in market cap on the earnings news, the biggest single increase on record, and now stands just shy of $2 trillion in value. Who knows if we are in bubble territory, there are certainly parallels that can be drawn to 2021, however, it is clear that Nvidia is backing up the hype with very strong earnings growth and product demand.

There is positive news in the UK as energy bills are set to fall to their lowest levels in two years. From the month of April energy regulator Ofgem are set to cut the price cap by around 12%, equating to an average saving of almost £240 per household. This will be the lowest level since prices were raised as a consequence of Russia’s invasion of Ukraine in February 2022. Ofgem however are still facing the issue that a record £3.1bn remains in unpaid bills. Energy prices have been a significant contributor to rising inflation and as this continually falls, investors believe this could help bring inflation down to target of 2% by June.

Eurozone inflation has continued to ease as headline inflation (year-on-year) fell to 2.8% in January. Expectations of an ECB rate cut have recently been pushed back to May and it’s estimated the ECB won’t cut rates before the US Fed.

It’s been a fascinating week in markets, which was dominated by the results of one single company, Nvidia. Their recent success helped propel the majority of global indices higher as the belief around the artificial intelligence revolution increases. With such a high profile company posting significant gains there is likely to be an element of “FOMO” (fear of missing out), however, we continue to believe a well-diversified portfolio, across a range of asset classes remains appropriate. This will of course include Nvidia, alongside many other positions, and ensures portfolio performance is not dictated by one company.

Nathan Amaning, Investment Analyst

Risk warning: With investing, your capital is at risk. The value of investments and the income from them can go down as well as up and you may not recover the amount of your initial investment. Certain investments carry a higher degree of risk than others and are, therefore, unsuitable for some investors.

Economic indicators pointed to continued expansion, although concerns about inflation and the potential for central bank tightening measures persisted. It was these concerns that weighed on fixed income markets, pushing yields higher (and prices lower). During the month of January, inflation data from the US and UK came in higher than expected. US headline inflation rose from 3.1% to 3.4% (year-on-year), while UK inflation rose for the first time in 10 months, from 3.9% to 4%. This data knocked the wind out of the ‘inflation is defeated’ sails and led investors to question whether the optimism of November and December was merited. The short-termism of markets currently leads to heightened volatility and market movements around key data releases, such as inflation. While these inflation prints in January were higher than expected it is worth remembering that inflation in January 2023 was 10.1% in the UK and 6.4% in the US – the trend has very clearly been towards lower inflation.

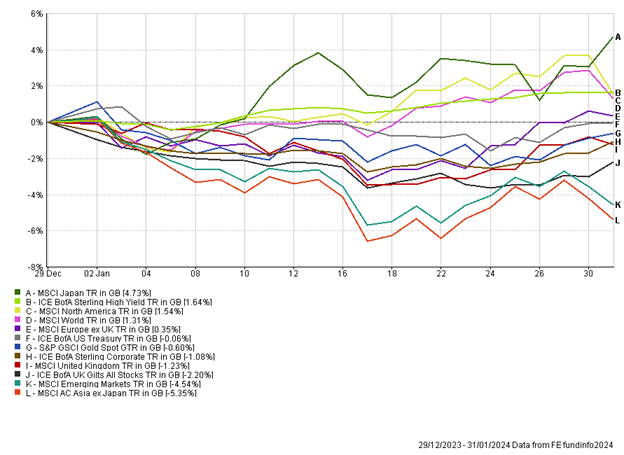

Equity performance in January was more varied, with countries such as Japan and the US performing well, while China was a clear laggard. We witnessed Japanese equities hit their highest levels since 1990, driven by the large cap exporters which have benefitted from significant weakness in the Japanese Yen. The more domestically focused mid and small cap stocks in Japan didn’t keep pace, although it is possible that the rally will broaden out which will benefit these smaller companies. At a domestic level inflation seems to be under control while interest rates remain in negative territory – a complete outlier in developed markets! Valuations continue to look compelling in many parts of the Japanese equity market and more shareholder friendly management teams has led to an improvement in profitability and dividends. Japan has also benefitted from investor flows which are now diverting from China and going to the other large, liquid markets in Asia such as Japan and India.

US equity markets hit fresh all-time highs towards the end of the month, two years after the previous highs. US economic data continued to highlight the resilience of the economy, with Q4 GDP reported at 3.3%, higher than the 2% expected growth. The labour market continued to add jobs at a pace, with the government and healthcare sectors two of the biggest contributors to hiring. The US government continues to spend spend spend, running aggressive budget deficits. Quite how sustainable this is remains to be seen, but in the short-term it is helping offset the negative impacts from higher interest rates. Unlike 2022, when sectors such as technology were hit extremely hard due to rising interest rates and bond yields, the technology sector so far helped power on the US market.

The artificial intelligence trend is gathering momentum, with investors pouring money into the perceived beneficiaries, such as Nvidia and Microsoft. We’ve now witnessed Microsoft become a $3 trillion company and surpass Apple as the largest US listed company. The concentrated US market, with a handful of the largest companies accountable for the lion’s share of market gains makes it difficult for a diversified approach. By its very nature diversification sees risk spread across a whole range of stocks, while with hindsight the best approach would have been to hold a few companies in size and nothing else. This is an inherently risky strategy and over the long-term would likely provide significant volatility and difficult periods. The excitement around the “magnificent seven” tech-focused stocks continue to grow, which is likely to lead to more capital inflows into them in the near-term. However, it is important to keep discipline and structure in approach to these companies and be wary of both the investment opportunity, but also valuation risk. History has shown us countless times that overpaying for investments is a punishing strategy. We have exposure to all of the aforementioned stocks but blend these companies with a wide range of other equity investments across the globe.

The weak spot in the US market in January was the regional banks, which fell significantly. There continues to be concerns over their exposure to commercial real estate, particularly the office sector, which is seemingly going through the same struggles the retail sector went through a decade ago, with office valuations falling by around 25% in 2023.

China’s woes continued in January, with the equity market suffering steep declines. The property sector has been under pressure and there seems to be little sign of improving. Sentiment was further knocked towards the end of the month with Chinese property developer Evergrande being ordered to liquidate, the company had more than $300bn of liabilities. The weakness in the stock market is likely to cause serious issues for Xi Jinping and we did witness the government step in to try and stimulate the market with various policies including limiting short-selling and allowing their wealth fund to increase purchases of Chinese equity ETFs.

The general outlook for the global economy has been trending up, with the market assigning a higher probability for a so-called soft landing. Companies are expected to grow earnings at meaningful rates in 2024 and 2025, while inflation should trend lower. The easing of interest rates should, in theory, be supportive for a range of asset classes. We continue to tread a careful path, mindful of risks, but equally seeing opportunities across a broad range of investments. Areas such as short-dated corporate and government bonds should offer positive real returns with limited interest rate sensitivity, while areas of the equity market trade on low valuations, which is historically very positive for long-term returns.

Andy Triggs

Head of Investments, Raymond James, Barbican

Risk warning: With investing, your capital is at risk. Opinions constitute our judgement as of this date and are subject to change without warning. Past performance is not a reliable indicator of future results. This article is intended for informational purposes only and no action should be taken or refrained from being taken as a consequence without consulting a suitably qualified and regulated person.

Appendix

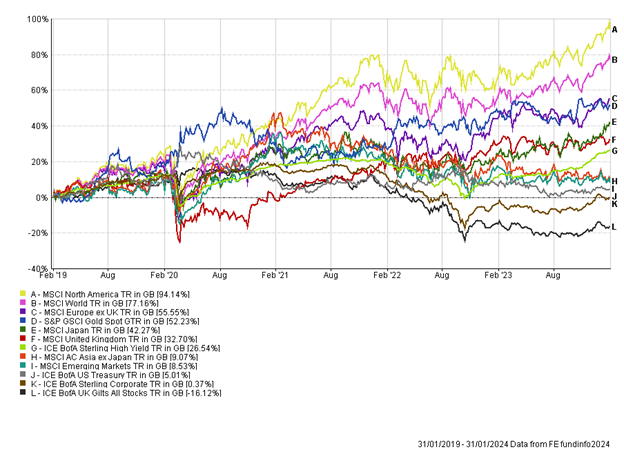

5-year performance chart

At the start of January 2023, Prime Minister Rishi Sunak made five promises, one was to grow the economy. We are in a pivotal year for the Conservative party, and this failed promise may be one of the reasons the party lose the upcoming general election. There are various reasons for the slowdown at the end of 2023; industry strikes were prevalent, poor weather kept shoppers’ home and the list goes on. The March Budget is less than three weeks away and may be one of the last chances that the Prime Minister and Chancellor get to turn the tide in favour of the Conservatives.

Politics is not our area of expertise so let’s turn back to UK inflation data which was released the day before on Wednesday. Headline inflation (year-on-year) held steady at 4% despite market expectations of a slight rise and the same was the case for core inflation, (excludes food and energy prices) reported at 5.1%. Inflation is certainly at its sticky point and the Bank of England (BOE) must consider this before their next meeting. UK wage growth (excluding bonuses) is trending lower but still running at 6.2%. This is still double the pace that the BoE would deem acceptable to bringing inflation down to the 2% target. There were some positives in the inflation report, with food prices falling on a month-on-month basis for the first time in two years.

Valentines day was celebrated on Wednesday and this day was chosen as a tactical strike day. Delivery food drivers for companies such as Deliveroo and Uber Eats staged a strike in demand for better pay and conditions. It involved up to 3,000 drivers and riders who are generally classified as self-employed, meaning their employers are not obliged to pay them the national living wage of £10.42 an hour. This wage will be rising in April and the workers want to be compensated for the “cold, rain and absurd distances” that they have to brave. On Friday morning UK retail sales shocked the market, with January’s data showing the biggest recovery in retail sales since April 2021 with people buying more across all categories except clothing. This, coupled with positive results from companies such as NatWest led the market higher on Friday and capped off a good week for UK equities.

Inflation in the US was a shock to markets as inflation came in hotter than expected, contradicting UK data. For January the inflation rate (month-on-month) rose to 0.3% and core inflation rose to 0.4%. This data disappointed and markets began to sell off, the S&P 500 dropped 1.4% on the Tuesday. The story of the US economy has been a defiant one as it remains robust, and this has meant expectations of rate cuts have firmly been pushed to the US Federal Reserve’s May meeting rather than March. In both the US and UK, the last mile for inflation is proving the toughest. The Russell 2000 index (US small cap index) proved particularly volatile this week, falling over 4% on the back of the higher inflation data. However, it has also experienced some very positive days of late and over the last five trading sessions is still in positive territory.

Recession has also arrived in Japan as they contracted at the end of 2023. GDP growth over Q4 2023 was -0.4%, a complete blow to investor expectations of 1.4%. The road to economic recovery in Japan will surely begin when the central bank decide to exit their decade long ultra-loose monetary policy. Weak domestic demand however makes it difficult for the Bank of Japan (BoJ) to pivot towards monetary tightening as they plan to do so by April. Large cap Japan stocks have performed extremely well during this period helping drive the Nikkei 225 index up 15% year to date. This has been offset by a weakening yen which has fallen over 5% versus GBP.

While Q4 2023 data was disappointing, more recent data suggest economies are re-accelerating which has spurred on hopes of very mild recessions and future growth. This combined with lower rates and falling inflation is the bull case for equities. We are positioned for this, but equally hold a range of assets that should benefit if this base case does not occur.

Nathan Amaning, Investment Analyst

Risk warning: With investing, your capital is at risk. The value of investments and the income from them can go down as well as up and you may not recover the amount of your initial investment. Certain investments carry a higher degree of risk than others and are, therefore, unsuitable for some investors.

China is facing three main problems; persistent disinflation/deflation that we mentioned above, the collapse of their stock market, which is down around 60% over three years and a falling property market. The world’s second largest economy has struggled to effectively stimulate the economy following the end of the COVID curbs in 2022 and the emphasis is really on the Chinese government to provide a solution.

Catherine Mann, a member of the UK Monetary Policy Committee (MPC) spoke this week and revealed her vote was to raise interest rates by 25bps (0.25%) to 5.5%. Her reasoning included the prospects of real incomes rising, continued tightness in the labour market and geopolitical events such as the attacks on the Red Sea trade route having the potential to raise UK inflation once again. The MPC is split over decisions on the base rate and investors have shifted views on the first rate cut to May 2024.

In the US, weekly jobless claims, the number of Americans filling for unemployment benefits, fell to 218,000, slightly below market expectations of 220,000. It’s interesting that high profile layoffs have not led to a surge in claims, likely meaning workers seem to be easily finding new jobs. Large tech companies such as TikTok, Amazon and Google have cut their working staff and most recently, Frontdesk, a US-based tech startup, fired 200 employees over a 2-minute Google meet call. Good news of sustained labour market strength weakens the case for the US Fed to cut rates in March, again moving expectations to May.

Uber Technologies is a brand that needs no introduction with its popular taxi service and food delivery service worldwide. Just this week Uber reported their first operating profits as a listed company, a pivotal moment for the company after their aggressive expansion plans paid off. The US firm reported $1.1bn profit in 2023 and we saw a 1% rise in the share price on Wednesday, now valuing the company at $147bn. Next week, Uber CFO is set to announce whether Uber will buy back shares or even pay out a dividend to investors.

The political elections continue this week as voters in Pakistan headed to the polls on Thursday. Strangely, the Ministry of Interior in Pakistan announced the suspension of mobile phone cellular services nationwide to “maintain the law-and-order situation”. Understandably this enraged the nation, with events described as an attempt by those in power to manipulate the election outcome. Former Prime Minister, Imran Khan, has already been jailed and barred from the ballot for corruption.

We have often said predicting the future is impossible and recent world events prove this. Diversification is as key as ever as we continue to shape portfolios. While we monitor and review markets on a daily basis, we prefer to focus on the long-term (multi-years) when it comes to strategic decision making.

Nathan Amaning, Investment Analyst

Risk warning: With investing, your capital is at risk. The value of investments and the income from them can go down as well as up and you may not recover the amount of your initial investment. Certain investments carry a higher degree of risk than others and are, therefore, unsuitable for some investors.

The Bank of England met on Thursday afternoon, holding interest rates firm at 5.25%. It was expected that this first meeting of the year was too soon for any rate cuts to occur and only one Monetary Policy Committee member (MPC), Swati Dhingra opted for a cut. The voting was a three-way split as two members voted for a 25bps rise while the final six voted to keep rates stable. Governor Bailey mentioned there had been a “shift in the BoE’s thinking” towards inflation, unemployment and wage growth levels needed to be achieved before a pivot on policy; this led to investors pushing back expectations of a first rate cut to May.

The eurozone has narrowly avoided a recession with Q4 2023 growth coming in flat at 0%. Market expectations were that GDP would be negative at -0.1% and this was based on the two largest economies, Germany and France, contracting and posting no growth. The belief among investors is that the European Central Bank (ECB) will only cut rates at their next meeting if the US Fed cut rates over fears of devaluing the Euro. It seems evident that the ECB need to make a move in order to stimulate the eurozone.

On a more positive note, German inflation eased more than expected to 2.9% after December’s anticipated anomaly rise. Germany is the largest energy consumer in the Eurozone with high energy prices burdening their manufacturing industry however the recent drop in energy prices contributed to the fall in inflation. There will be another inflation print before the ECB’s next meeting in March so a falling trend could spur the ECB to make their move.

Germany and France are alike in another matter as both countries are seeing protests from farmers. There is a phrase “no country riots quite like the French” and the farmers are no exception. French farmers blocked major highways around Paris over pay disputes. Inflationary pressures have raised the costs of major inputs such as energy, fertiliser and transport and this has now been added to by excessive regulation. This put immediate pressure on newly appointed PM, Gabriel Attal, and he announced the scrapping of diesel tax increases for farmers and extra steps to reduce red tape on farmers.

Earnings season continued in the US and we saw mixed results from the so-called ‘Magnificent Seven’. Meta (Facebook) and Amazon posted better than expected results, with Meta even initiating a dividend, which sent share prices soaring after-hours. Apple’s results were underwhelming with concerns around China leading to growth fears; shares in the $3 trillion company dropped over 2% in after-hours trading.

US Non-Farm Payrolls data has just been released and surprised to the upside as 353,000 jobs were added to the economy in January. This came in almost double market expectations of 180,000. The continued strength of the labour market highlights the current resilience of the US economy and caused investors to question whether the Fed will need to cut rates in the near term. We witnessed US government bonds sell-off on the news.

On Thursday Formula One driver Lewis Hamilton, announced his decision to leave Mercedes at the end of the 2024 season, joining rivals Ferrari. The announcement of the seven-time world title winner joining coupled with a positive earnings report sent Ferrari stock up 11%, reaching an all-time high. The right driver in the right team can be a very powerful combination and indeed reflects some of the qualities we look for when selecting fund managers for our portfolios. We believe the right investment team is important, but that team must also operate in the right business (culture) in order to maximise and sustain performance.

Nathan Amaning, Investment Analyst

Risk warning: With investing, your capital is at risk. The value of investments and the income from them can go down as well as up and you may not recover the amount of your initial investment. Certain investments carry a higher degree of risk than others and are, therefore, unsuitable for some investors.

In the first Monthly Market Commentary of the year, Raymond James European Strategist, Jeremy Batstone-Carr, looks back on the largely positive start to the year for many of the world’s leading markets, the struggles of the Chinese economy, and areas for investors to consider for the coming months.

![]()