I was pleased to be able to meet many of you earlier in February, albeit only virtually. I was even more pleased to hear Andy Triggs, Head of Investments at Raymond James, Barbican, say he wasn’t going to make any predictions about how the then-tense stand-off on the Ukrainian border would play out.

At the time, there were many grand, serious-sounding geopolitical strategists confidently claiming that Putin was bluffing. They are now busy washing their faces, while Andy’s remains reassuringly egg-free.

That’s one good reason not to make such predictions, and particularly not to invest off the back of them. Life is complex; things that shouldn’t happen frequently do. But he also set out another reason: Even if you’re right, markets often do the exact opposite to what you’d expect.

I talked about this in the December note: How markets can appear psychopathic, sometimes reacting positively to bad news. Those of you on the call will remember we ran through some geo-political events from the past, showing how the markets’ shock can be surprisingly short-lived. The instance that stands out for me, because I remember it well, was the day the second Gulf War began in 2003. Having fallen more-or-less constantly following the tech burst in 2000 and then the 9-11 attacks, markets actually rose that day, marking the start of a bull market (i.e. rising prices) that lasted four years.

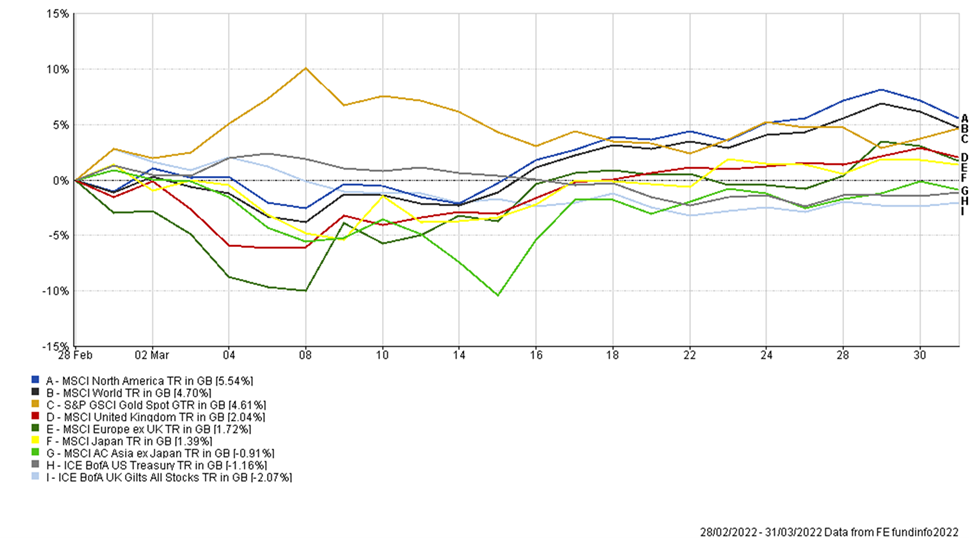

And so it was in February. As you can see from the chart, European markets sold off on the 24th February, the first day of the invasion, but US markets rose and, by Monday, European markets were back where they started. It’s hard to know for certain why this happens, only to say that markets hate uncertainty (which is why they had been steadily falling for weeks) and Putin’s actions – unfortunately – ended any uncertainty about whether Russia would invade.

That’s not to say markets won’t yet begin to fall again. They’ve remained volatile into March, and no doubt will do so for some time to come. (Predicting that “markets will be volatile” is one of the few safe predictions in investing, which is why so many of us commentators predict it. It’s like telling people to “expect weather”). We’ve simply traded one uncertainty; will Russia invade Ukraine? for others; will Russia invade a NATO country? So this is very far from an all-clear on the investing front.

Another theme we’ve expounded on at length is inflation and its likely impact on interest rates. This is so important for your finances; almost everything else is noise, which is why we spend so much time on it. So in last month’s note we covered the rotation within markets: How everything that had performed well for the last ten years – when inflation was falling – had started to do badly, while everything that had done badly had started to perform well. And all because of inflation’s comeback tour.

Well, it’s all started to rotate back the other way again. And it’s due to what’s happening in Ukraine. You can see in the chart that government bonds (called gilts in the UK, and Treasuries in the US), which hate inflation, continued to fall in the first two weeks of February, but as invasion concerns mounted, they started to rally.

Partly this is because investors use these bonds as financial safe havens in times of stress, often selling riskier assets, like shares, in order to buy them. This pushes the prices of bonds up, and shares downwards.

But it’s also because investors are concerned that the war in Ukraine might lead to a slowing of economic activity, which means central banks are now less likely to raise interest rates to put the brakes on. This too is positive for bonds, but potentially bad news for shares.

Although, as always, it’s never quite as simple as that. Shares don’t like the fact that war might slow the economy, but they do like Central Banks’ responses. But what it has meant so far is that many of the parts of the stock market that had collapsed in January, most notably technology shares, have sprung back to life again. While some areas that had rallied, like European banks, have slumped. The rotation, in other words, is rotating.

But even that’s not that simple. Energy prices, which performed well in January, performed well in February too. So that part of the initial rotation continues. This is due to the threat of a cut in supply from Russia. This too then plays back into the inflation story, as higher energy costs feed into rising prices too. This potentially puts us on a path to stagflation – a grim combination of slowing economic growth and higher inflation. Hardly any assets like this scenario, and may explain why the rally in bond prices was somewhat muted given the severity of the news.

One set of assets that has, unsurprisingly, been walloped are Russian shares, bonds and the rouble. Sanctions, primarily those stopping Russia’s central bank from selling its piles of dollars and euros, have caused the rouble to collapse. Thankfully your portfolios have precious little exposure to anything Russian, so the direct effect of this to you is negligible.

Finally, as you can see from the chart, gold has been a useful investment for us this month. Gold can be a capricious beast. We hold it as insurance, but, like many insurance contracts, you can never be quite sure what it’ll pay out on until after the event. Thankfully, this event seems to be covered, and its rising price has helped your portfolio to weather this storm.

All this paints a highly confusing picture. We do not know how these events will play out – nobody does, and you should treat with caution anyone who claims they do. It’s no time for glib “I’m-sure-it’ll-all-be-fine” statements either – we’re as concerned about the world as I’m sure you are.

In the face of this, and in respect of your capital, we believe balance and diversification are the best options. Placing your assets into a single asset or market based on a prediction risks too much if that prediction proves wrong. And as events have shown, trying to predict the actions of a man like Putin is likely to end badly.

Simon Evan-Cook

(On Behalf of Raymond James, Barbican)