Many of our readers will no doubt be aware that this week has been historic for all the wrong reasons, with Russia invading Ukraine. We know it is a difficult time and our thoughts are with those people affected by these events.

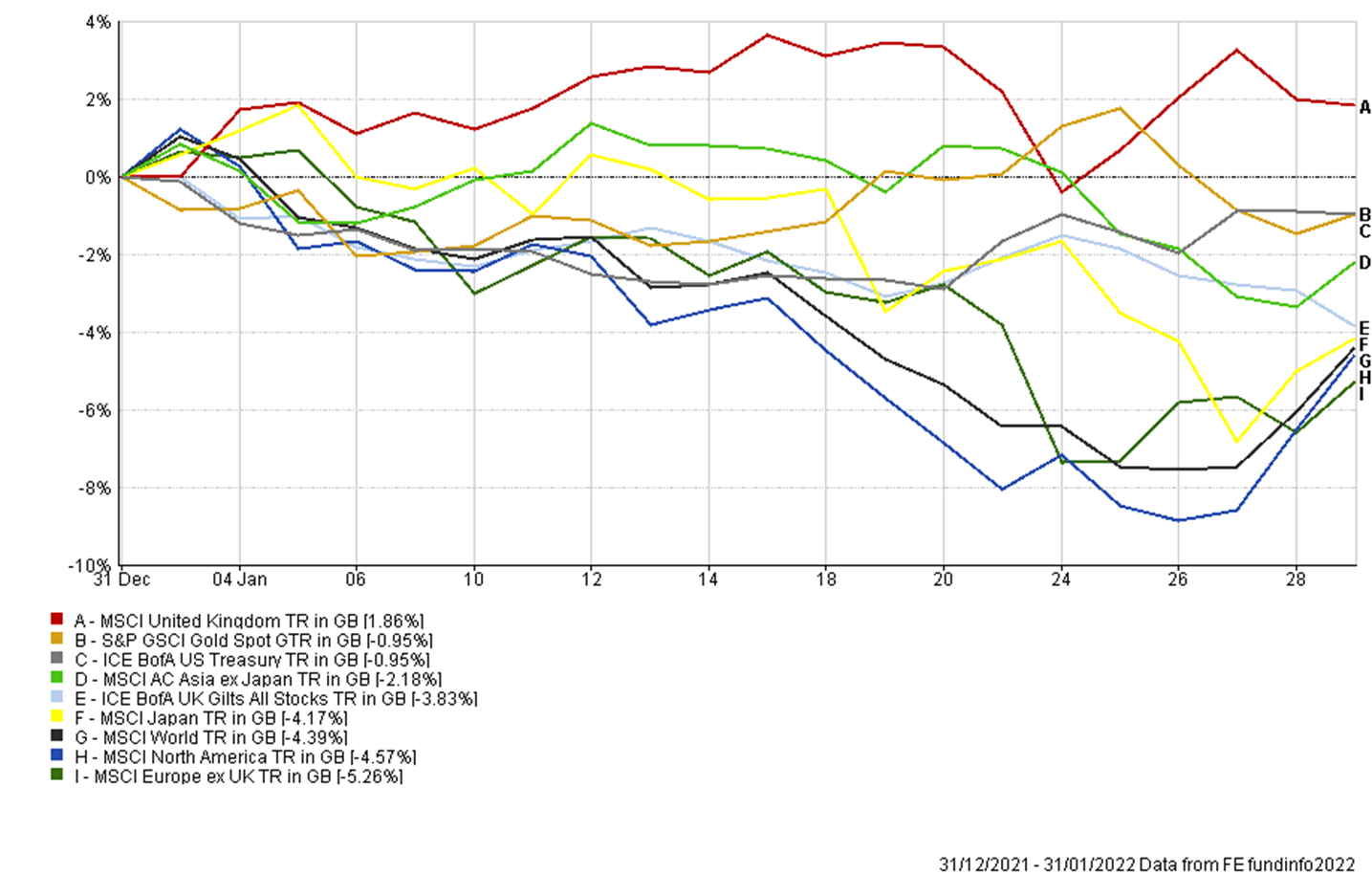

Focusing on the impact on markets, we have seen big swings in global equities this week. It’s worth remembering that equity markets are typically forward-looking, and the potential geopolitical risks were in part already discounted into prices. However, it appears that the full invasion witnessed towards the end of the week was not ‘in the price’ and we saw European and Asian markets fall heavily on Thursday. The US equity market, after opening in the red, staged a remarkable comeback and actually ended the day up, with the S&P 500 closing 1.5% higher. Japanese equities rose by a similar amount overnight and UK and European equities are in positive territory today at the time of writing. At this stage, it’s not 100% clear what the endgame will be, and with that uncertainty still lingering, there is potential for asset prices to remain volatile in the short term.

Safe-haven assets have responded to the turmoil, with prices generally rising this week. Within bond markets, investors are beginning to question whether central banks will be able to raise interest rates as aggressively as expected, into what could be a slowing global economy. Other safe-havens such as gold and the US dollar also performed well. It’s a timely reminder of their insurance like characteristics and it is why they are held in our clients’ portfolios.

The oil price broke through $100 a barrel, climbing to eight-year highs on concerns around global supply. Russia produces around 11 million barrels of oil a day, much of which is exported, and this supply could be impacted if Western sanctions escalate. European natural gas prices also spiked; Russia currently supplies around 35% of Europe’s natural gas and again this supply could become strained. Rising commodity prices will do little to soothe concerns about inflation, although it should be remembered that higher energy prices act as a quasi-tax on the consumer and could have the effect of dampening demand for goods and services and this is deflationary.

There was some positive economic data released this week, although clearly this has been overshadowed by Russia’s invasion of Ukraine. Services and manufacturing PMI data for the UK came in ahead of consensus and US GDP for Q4 2021 was revised higher to 7%.

Periods, like we are going through now, are highly emotive and it can feel very difficult to be invested in asset markets. History has repeatedly shown us that these uncomfortable moments are often also opportunities, especially for investors with a long-term time horizon, who can look through the short-term headwinds. At an investment committee level, we try to do this in an objective, structured way to ensure we are making appropriate long-term decisions for the portfolios.

Andy Triggs | Head of Investments, Raymond James, Barbican

With investing, your capital is at risk. The value of investments and the income from them can go down as well as up and you may not recover the amount of your initial investment. Certain investments carry a higher degree of risk than others and are, therefore, unsuitable for some investors.