We woke to major news from domestic shores on Wednesday. Not only had England men’s football team announced the appointment of a new permanent manager, but UK inflation fell to 1.7%, the lowest level in three and half years and below the official 2% inflation target. Football fans will be hoping the new manager, Thomas Tuchel, will bring in a new brand of attacking football, while lower than expected inflation should allow for a new era of lower interest rates for the UK economy.

There were question marks around when the Bank of England (BoE) would next lower interest rates, however the inflation data has led to an interest rate cut being nailed on at the next meeting on 7th November. There is also the possibility for a further cut during December. Not only did headline inflation fall, but core (which excludes food and energy) was lower than expected, as was services inflation, falling below 5% for the first time since May 2022. All this data should empower the BoE to take action and reduce rates imminently.

The European Central Bank (ECB) has its foot firmly on the easing accelerator as they delivered their third successive interest rate cut on Thursday. Economic growth in the Eurozone is stalling, with Germany in particular struggling. This coupled with falling inflation, last reported at 1.7%, has given the ECB scope to continue to lower interest rates in an effort to support the broader economy.

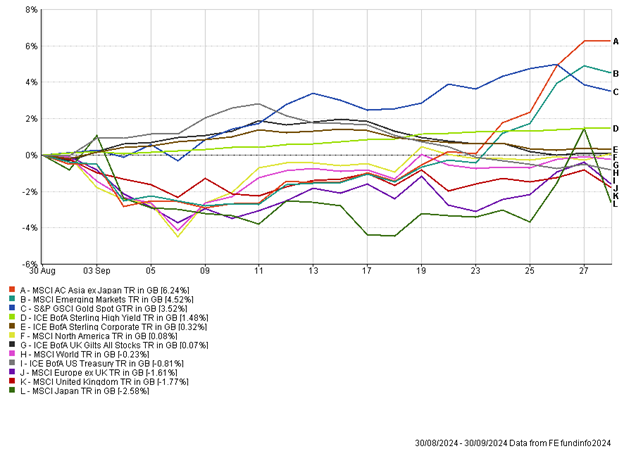

Chinese equities have sold off over the course of the week as investors have soured on the potential impact of the stimulus measures announced at the end of September. There has most likely been an element of profit taking by investors, with the main Chinese equity index rallying over 30% following the stimulus announcements. In terms of economic data, Chinese inflation was released on Monday morning, and showed that the country continues to flirt with deflation. Headline inflation was only 0.4% year-on-year and will continue to alarm policy makers who will be keen to avoid a deflationary slump.

US retail sales were strong for September, with the data beating expectations. The data points to a resilient consumer and may deter the US Fed from cutting rates too aggressively. In the aftermath of the data US government bond yields rose (prices fell), moving above 4% on the US 10-year bond. This was a role reversal to the UK 10-year government bond, which performed well this week with the 10-year UK government bond yielding less than its US counterpart.

The race to the White House continues to intensify as the 5th November looms closer. In what is expected to be a very tightly contested race, Donald Trump moved ahead of Kamala Harris in the betting markets this week. This contradicted recent polls which showed Kamala Harris as the most likely future President. Despite the uncertainty over who will be the future leader, US equity markets continued a recent strong streak, pushing higher. After underperforming over the summer months, the large cap tech and artificial intelligence (AI) stocks pushed higher. Nvidia, has hit a new all-time high this week, after breaking levels last seen at the end of June 2024.

Company results linked to AI and chip manufacturing provided mixed messages. The Dutch behemoth ASML released its results this week and provided a weaker outlook for 2025, leading to a 15% drop in its share price. To add to its woes, the quarterly results were published early, in an error. Taiwan Semiconductor Manufacturing Company (TSMC), the world’s largest contract chipmaker, released strong Q3 earnings and pointed to a bright outlook for its business, due to soaring AI-demand.

Gold has continued to advance this week, once again making new all-time highs. Silver, also advanced, reaching $32 an ounce. This is still considerably lower than its level in 2011 when it reached $50.

With developed market equities grinding higher and UK government bonds performing well on the back of softer inflation it was a pleasing week for portfolios, making new highs for 2024. Portfolios remain well diversified which we think is sensible given the elevated level of uncertainty at a macro level.

Andy Triggs, Head of Investments

Risk warning: With investing, your capital is at risk. The value of investments and the income from them can go down as well as up and you may not recover the amount of your initial investment. Certain investments carry a higher degree of risk than others and are, therefore, unsuitable for some investors.